CIO comments on RBI Bi-monthly Policy June 2018

#

7th Jun, 2018

- 1780 Views

NDNC disclaimer: By submitting your contact details or responding to Bajaj Allianz Life Insurance Company Limited., with an SMS or Missed Call, you authorise Bajaj Allianz Life Insurance Company Limited and/or its authorized Service Providers to verify the above information and/or contact you to assist you with the purchase and/or servicing

RBI hikes rates, but maintains status quo on policy stance

The RBI Monetary Policy Committee (MPC) hiked the policy rate by 25 bps (with all MPC members voting for a rate hike). However, it maintained its ‘neutral’ monetary policy stance.

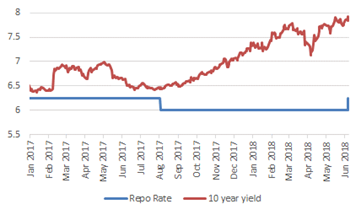

RBI Repo Rate Vs 10 year yield

Source: Bloomberg

RBI revised the CPI headline inflation forecast for H1 FY19 to 4.8-4.9% (from the earlier forecast of 4.7-5.1% in April policy review), and for H2 FY19 to 4.7% (from the April forecast of 4.4%)—with risks tilted to the upside. The revisions in inflation target is attributed to the following:

However, the central bank highlighted various risks to the inflation target, particularly from the hardening of crude oil prices, which seems durable, although uncertainty remains on it—to the upside as well as the downside. Other risks include uncertainty in global financial market developments, rise in household inflation expectations, staggered impact of HRA revisions by state governments, MSP hike impact on kharif crops, and progress of monsoons.

On the economic front, the RBI has retained the April GDP forecast of 7.4% (with risks evenly balanced), after the robust Q4 FY18 GDP growth of 7.7%YoY reported recently.

Market Outlook:

Long term bond yields have hardened post the policy announcement, with market consensus earlier around no rate hike, but a probability of change in policy stance. However, with the RBI keeping its policy stance unchanged at ‘neutral’, we feel that future rate action and policy stance will continue to be data dependent, and especially track the course of inflation & oil price trajectory, and global monetary policy events. We continue to prefer the shorter end of the yield curve at this juncture.

The positive factor is that RBI has maintained its GDP forecast for FY19, and remains upbeat on the domestic economy—by commenting that it has exhibited sustained revival in recent quarters, and particularly investment activity has recovered well, and could be boosted further from resolution in distressed sectors by the Insolvency and Bankruptcy Code (IBC). This bodes well for equities, although we do have some macro headwinds in the form of higher crude oil prices, rising interest rates, and unwinding of global easy monetary policy. Investors should continue to invest systematically in equities, with our preference being for large-cap funds.

Enter your email address to subscribe to this blog and receive notifications of new posts by email.

Facebook

Twitter

pintrest

instagram

Whatsapp

Linkedin

More