RBI hikes repo rate by 35 bps as expected but was a bit hawkish on the margin

#

7th Dec, 2022

- 10033 Views

NDNC disclaimer: By submitting your contact details or responding to Bajaj Allianz Life Insurance Company Limited., with an SMS or Missed Call, you authorise Bajaj Allianz Life Insurance Company Limited and/or its authorized Service Providers to verify the above information and/or contact you to assist you with the purchase and/or servicing

Comments from Mr. Sampath Reddy, Chief Investment Officer, Bajaj Allianz Life

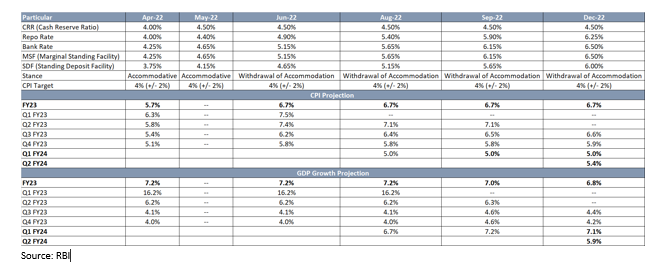

RBI’s Monetary Policy Committee (MPC) hiked the benchmark policy rate (repo rate) by 35 bps to 6.25%. 5 out of 6 MPC members voted in favour of hiking the Repo rate by 35 bps while 1 member voted against the repo rate hike. The marginal standing facility (MSF) rate and the Standing Deposit Facility (SDF) rate stands adjusted to 6.50% & 6.0% respectively. Cash Reserve Ratio (CRR) remained unchanged at 4.50%. RBI maintained its policy stance of ‘withdrawal of accommodation’ to ensure that inflation remains within the target going forward, while supporting growth. 4 out of 6 MPC members voted in favour of “withdrawal of accommodation” stance while 2 members voted against this resolution.

The RBI governor also stated that Inflation has remained at or above the upper tolerance band since January 2022 and core inflation is persisting around 6%. Headline inflation is expected to remain above or close to the upper threshold in Q3 & Q4 FY23. It is likely to moderate in H1FY24 but will still remain well above the 4% target. With the inflation rate expected to be elevated at 6% in H2FY23 and with liquidity still in surplus, overall monetary and liquidity conditions remain accommodative, despite the 225 bps of cumulative rate hikes (April-Dec).

On the domestic economic front, the RBI has mentioned that the economic activity continued to gain strength as urban consumption firmed up further, driven by sustained recovery in discretionary spending, especially on services such as travel, tourism and hospitality. Other high frequency indicators of Indian economy are also showing sustained recovery. Going ahead, investment activity will get support from government capex. Indian economy remained resilient in the midst of distressing global macroeconomic environment. However, the RBI governor also mentioned that in an interconnected world, we cannot remain entirely isolated from adverse spillovers from the global slowdown and its negative impact on our net exports and overall economic activity. The key risks to the outlook continue to be the headwinds emanating from extended geopolitical tensions, global slowdown and tightening of global financial conditions. On this backdrop, real GDP is expected to be 6.8% in FY23 vs 7% earlier.

On the inflation front, the central bank said that the adverse climate events – both domestic and global – are increasingly becoming a significant source of upside risk to food prices. Global demand is weakening. Geopolitical tensions continue to impart uncertainty to the food and energy prices outlook. The main risk is that core inflation (CPI excluding food and fuel) remains sticky and elevated at ~6%. The RBI kept inflation projection unchanged at 6.7% FY23, with risks evenly balanced. For Q1FY24 & Q2FY24, the RBI expects CPI inflation at 5% & 5.4% respectively.

On the liquidity front, the RBI said that in the period ahead, liquidity conditions are likely to improve due to several factors which would include moderation in currency in circulation in the post-festival period, pick up in government expenditure in the last few months of the financial year and higher forex inflows due to the return of portfolio investors. However, the RBI governor also mentioned that market participants must wean themselves away from the overhang of liquidity surpluses which means market should be prepared for further tighter liquidity condition.

Outlook:

The policy seemed slightly hawkish on the margin and indicated that there may be space for further tightening, although it will depend on the inflation trajectory and the terminal rate for the US Federal Reserve. The RBI’s policy was in line with expectations of a 35 bps rate hike (highest policy rate since August 2018). However, the RBI kept the policy stance unchanged at “withdrawal of accommodation” although some segments of the market were expecting a change in stance. India’s economic growth forecast, inflation outlook and currency depreciation stands better placed than peer emerging economies.

We believe this strong positioning of India will help us in dealing with the prevailing global inflation-growth challenges better.

Globally, we have seen central banks engaging in aggressive monetary tightening to deal with multi-decade high inflation. With the macro situation and especially the inflation scenario relatively better placed in India, we feel that the RBI may be nearing the end of the rate hike cycle in India.

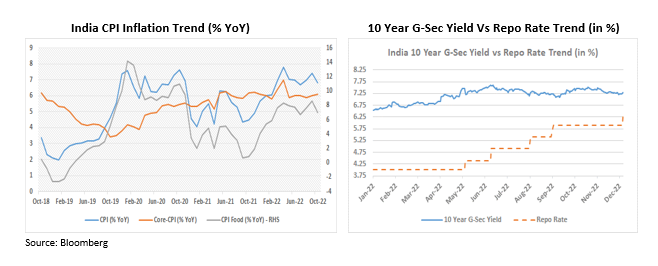

Post the policy announcement bond yields hardened a bit. With corporate bonds spreads still being very tight, we may witness some widening in spreads going forward. From a fixed income perspective, we prefer the short-medium part of the yield curve.

Disclaimer: “The views expressed by the Author in this article/note is not to be construed as investment advice and readers are suggested to seek independent financial advice before making any investment decisions”

Enter your email address to subscribe to this blog and receive notifications of new posts by email.

Facebook

Twitter

pintrest

instagram

Whatsapp

Linkedin

More