CIO comments on RBI Bi-monthly Policy, December 2018

#

5th Dec, 2018

- 2926 Views

NDNC disclaimer: By submitting your contact details or responding to Bajaj Allianz Life Insurance Company Limited., with an SMS or Missed Call, you authorise Bajaj Allianz Life Insurance Company Limited and/or its authorized Service Providers to verify the above information and/or contact you to assist you with the purchase and/or servicing

RBI keeps policy rate & stance unchanged, but slashes inflation projection – giving a dovish undertone

As expected, the RBI Monetary Policy Committee (MPC) kept the policy repo rate unchanged (with all MPC members unanimously voting for the same). It also kept the monetary policy stance unchanged at “calibrated tightening”, although one MPC member voted to change the stance back to “neutral”.

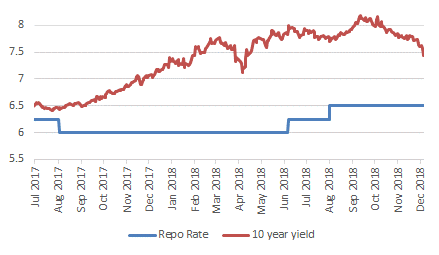

RBI Repo Rate Vs 10 year yield

Source: Bloomberg

With CPI headline inflation coming in below expectations recently, the central bank cut the inflation forecasts quite substantially. CPI headline inflation forecast for H2 FY19 has been cut from 3.9-4.5% in October policy to 2.7-3.2% in this policy, while RBI forecast CPI headline inflation for H1 FY20 at 3.8-4.2% in this policy (compared to forecast of 4.8% for Q1 FY20 in the October policy).

However, with the downward revision in inflation trajectory, RBI has highlighted some upside risks & uncertainties—such as possible reversal in unusually low prices of certain food items (esp. perishable items), uncertainty of MSP impact on inflation, uncertainty on medium term outlook for crude prices, volatility in global financial markets, and fiscal slippages at centre/state level.

On the economic front, despite the recent Q2 FY19 GDP numbers coming in below expectations, the central bank retained the GDP forecast for FY19 at 7.4%–with risks somewhat to the downside.

Market Outlook: The overall tone of the policy was a bit dovish, with inflation forecasts being cut substantially. The bond markets reacted positively, and the 10 year yield closed at 7.44%–down 13 bps from yesterday’s close. RBI also announced Statutory Liquidity Ratio (SLR) cut by 25 bps from beginning of 2019 to 19.25%, followed by progressive cuts (of 25 bps) every quarter, until the SLR comes down to 18%. Although this will reduce appetite for government securities from banks who are presently sitting on excess SLR, it will be beneficial for banks who will have buffer to lend more—thereby benefiting credit growth.

With liquidity being tight within the system, the RBI has been proactive by announcing liquidity infusion through OMO (Open Market Operation) purchases. Liquidity tightness has eased a bit lately, and we expect that the central bank will continue to use the OMO route to manage liquidity. Also, the RBI governor indicated that if upside risks (mentioned in the policy) do not materialize, then it could open up space for future policy action—therefore keeping it data dependent. We had increased duration in our portfolios over the past month, and with yields having already factored in the outcome of the policy, we now prefer the shorter to medium term segment of the yield curve.

Enter your email address to subscribe to this blog and receive notifications of new posts by email.

Facebook

Twitter

pintrest

instagram

Whatsapp

Linkedin

More