CIO comments on RBI Bi-monthly Policy, 1 August, 2018

#

2nd Aug, 2018

- 1264 Views

NDNC disclaimer: By submitting your contact details or responding to Bajaj Allianz Life Insurance Company Limited., with an SMS or Missed Call, you authorise Bajaj Allianz Life Insurance Company Limited and/or its authorized Service Providers to verify the above information and/or contact you to assist you with the purchase and/or servicing

RBI hikes rates, and maintains status quo on policy stance, as broadly expected

The RBI Monetary Policy Committee (MPC) hiked the policy rate by 25 bps (with five MPC members voting for a rate hike and one voting against). It maintained its ‘neutral’ monetary policy stance, as broadly expected.

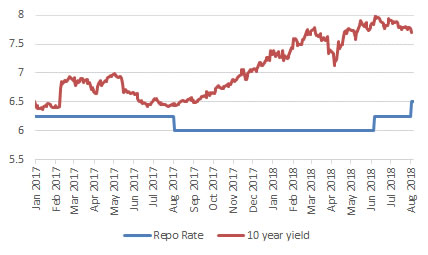

Source: Bloomberg

RBI revised the CPI headline inflation forecast marginally upwards for H2 FY19 to 4.8% (from the earlier forecast of 4.7% in June policy review), and the projection for Q1 FY20 is 5%—with risks evenly balanced. The central bank said that inflation outlook has been shaped by the following factors:

On the economic front, the RBI has retained the GDP forecast of 7.4% for FY19 (with risks evenly balanced), and projection for Q1 FY20 GDP growth is 7.5%. The central bank also added that rising trade protectionism poses a grave risk to near-term and long-term global growth prospects. Geopolitical tensions and elevated oil prices also continue to be the other sources of risk to global growth.

Market Outlook: RBI policy action was broadly along expected lines. What has probably been read favourably by the market (and led to some respite in bond yields) is that CPI headline inflation forecast for H2 FY19 has hardly been changed from the earlier monetary policy (only revised upwards by 10 bps), despite the MSP hikes. However, the RBI maintained that uncertainty still remains on the inflation front and it needs to be monitored closely.

We feel that future monetary policy action will continue to be data dependent. With the yield curve being flattish, we continue to prefer the shorter end of the yield curve.

Enter your email address to subscribe to this blog and receive notifications of new posts by email.

Facebook

Twitter

pintrest

instagram

Whatsapp

Linkedin

More